Market Overview

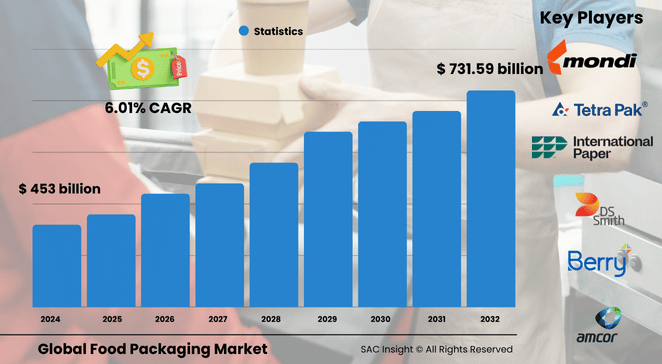

The global food packaging market size was roughly US$ 453 billion in 2024 and is on track to reach about US$ 731.59 billion by 2032, expanding at an average 6.1% CAGR over 2026-2032. First-hand industry insights point to three structural tailwinds: the explosive rise of online grocery and meal-kit services, tighter sustainability mandates that reward circular materials, and rapid advances in active and smart-pack technologies that lengthen shelf life. Deep market evaluation also shows consumption rebounding well past pre-pandemic levels as consumers gravitate toward portion-controlled, on-the-go formats. The U.S. food packaging market alone is projected to top US$ 154.94 billion by 2032, reflecting robust demand for tamper-evident and temperature-controlled solutions across e-commerce channels.

Summary of Market Trends and Drivers

• Surge in meal-delivery, quick-service restaurants, and convenience snacking is fuelling lightweight, resealable formats.

• Eco-conscious shoppers—and regulators—are accelerating the shift from virgin plastics to recyclable paperboard, bio-based films, and mono-material pouches.

• Smart indicators (freshness, temperature, tamper) and Modified Atmosphere Packaging (MAP) are gaining traction as brands race to cut food waste and extend shelf life.

Key Market Players

The report profiles global and regional leaders such as Amcor plc, Mondi, Berry Global, International Paper, Smurfit Kappa, DS Smith, Tetra Pak, and a rising cohort of specialty innovators focused on compostable resins and intelligent labels. Collectively, these firms set the competitive tempo through rapid material innovation, digital printing investments, and strategic MandA aimed at sustainable growth.

Key Takeaways

• Market value (2024): ~USD 453 billion

• Projected value (2032): ~USD 731.59 billion at a 6.1% CAGR

• Asia Pacific commands the largest market share at just over 40%.

• Flexible packaging leads by type, capturing roughly 44% of 2024 revenue.

• Plastics remain dominant by material (~39% share) but bio-based and paper solutions are the fastest-growing.

• Active, smart, and digitally printed packs are the top market trends shaping product design through 2032.

Market Dynamics

Drivers

• Rising demand for convenience and ready-to-eat foods among urban consumers.

• Growth of e-commerce and meal-kit subscriptions requiring durable, temperature-stable packs.

• Regulatory push for recyclable and compostable materials spurring innovation and market growth.

Restraints

• Volatile raw-material prices—especially polymers—squeeze converter margins.

• Complex, fast-evolving labelling rules create compliance costs for exporters.

Opportunities

• Edible and fully compostable films offer brand-differentiating sustainability credentials.

• Digital printing unlocks late-stage customisation, short-run economics, and eye-catching graphics.

Challenges

• Balancing barrier performance with recyclability remains technically demanding.

• Fragmented recycling infrastructure limits circular-economy claims in many emerging markets.

Regional Analysis

Asia Pacific dominates thanks to its vast population, booming organised retail, and rising frozen-food demand. North America follows, powered by high disposable incomes and fast adoption of premium, health-focused packaged foods. Europe’s strict circular-economy policies are forcing rapid material substitutions, while Latin America and the Middle East and Africa post steady gains on the back of expanding cold-chain networks.

• Asia Pacific: Largest share; rapid urbanisation and e-commerce spur single-serve packs.

• North America: Strong demand for meal-kits and smart, tamper-evident formats.

• Europe: Sustainability regulations drive paper-based and mono-material innovation.

• Latin America: Growth tied to canned and MAP-ready formats for longer shelf life.

• Middle East and Africa: Rising dairy and poultry consumption boosts chilled-food packaging.

Segmentation Analysis

By Type

• Flexible – Lightweight, space-efficient, >44% share.

Flexible pouches, films, and wraps dominate because they use less material, cut logistics costs, and support high-impact graphics—ideal for snacks, sauces, and frozen fare.

• Rigid – High protection, niche for shelf-stable goods.

Rigid cans, jars, and bottles safeguard products that need robust barriers or retort processing, such as beverages, condiments, and canned vegetables.

• Semi-rigid – Balance of strength and flexibility.

Trays and clamshells offer structure without the weight of full rigid formats, suiting fresh produce and ready meals.

By Material

• Plastics – Versatile, 39% market share.

PET, PE, and PP provide strong barriers and design freedom. Advances in mono-PE pouches and chemical recycling aim to close the loop.

• Paper and Paper-based – Fastest-growing eco-choice.

Recyclable coated paperboard and molded fibre appeal to consumers and regulators seeking lower-carbon options.

• Glass – Premium, inert, recyclable.

Favoured for sauces and beverages where flavor integrity and shelf presence matter.

• Metal – Long shelf life and high recycling rates.

Aluminium and steel cans remain critical for canned foods, offering robust protection and near-infinite recyclability.

• Others (bio-polymers, wood) – Emerging green alternatives.

PLA, PHA, and wood-based composites target zero-waste goals in niche applications.

By Packaging Format

• Bottles – 24% share, buoyed by dairy and functional drinks.

Lightweight designs and bio-based resins widen appeal.

• Cups – Convenience-driven, spill-proof.

Single-serve yogurts, desserts, and salads fuel growth.

• Pouches – Stand-up, resealable, custom shapes.

Ideal for baby food, soups, and pet treats; strong unit-growth outlook.

By Food Type

• Frozen Food – 29% share, needs high-barrier films.

Vacuum-sealing and MAP reduce freezer burn, catering to busy consumers.

• Chilled Food – Fresh perception, premium pricing.

Transparent, breathable films keep produce crisp while showcasing quality.

• Canned and Shelf-Stable – Reliability for long storage.

Metal and retortable pouches ensure safety without refrigeration.

By Application

• Bakery and Confectionery – 27% share.

Moisture-barrier films and eye-catching cartons drive impulse sales.

• Dairy Products – Aseptic and temperature-resistant packs.

Growth tied to flavoured milks, yogurts, and cheese snacks.

• Fruits and Vegetables, Meat and Seafood, Sauces and Dressings, Others

Each segment leverages tailored barrier properties to maximise freshness and minimise waste.

By End-user

• Chain Restaurants – Largest slice of demand.

Portion-controlled, brandable packs support delivery and takeaway.

Quick-service, cafés, full-service outlets, and FMCG brands round out demand, each pushing for cost-effective, sustainable solutions.

Industry Developments and Instances

• Nov 2024: A U.S. converter launched coated recycled paperboard tailored for food contact, advancing circular-economy goals.

• Oct 2024: New “RotiBag” introduced for hot grab-and-go foods, featuring anti-fog windows and curb-side recyclability.

• Sep 2024: Compostable flexible range debuted to tap surging demand for plastic-free snack packs.

• Jun 2024: Collaborative paper-based multipack solution rolled out for confectionery and biscuits, fully recyclable in household streams.

• Feb 2024: First all-polyethylene spouted pouch for yogurt hit U.S. shelves, combining high barrier with mono-material recyclability.

Facts and Figures

• Flexible formats account for ~44% of global revenue, the largest type segment.

• Asia Pacific captured >40% market share in 2024, led by China and India.

• Plastic remains dominant at ~39% of material demand despite sustainability headwinds.

• Digital printing can cut SKUs’ time-to-shelf by 30%, enhancing marketing agility.

• Only 9% of global plastic waste is recycled today, underlining the urgency for circular solutions.

Analyst Review and Recommendations

Our market analysis shows food packaging in a decisive transition from cost-driven to sustainability-led innovation. Players that pair high-barrier performance with recyclability or compostability will capture outsized market growth. Investment in mono-material laminates, digital printing, and active-pack sensors is strongly advised. Regionally tailored strategies—paperboard in Europe, smart MAP in North America, and lightweight pouches in Asia—will be critical to defend market share through 2032."